February rarely defines the year in Manhattan real estate, but it often shows where momentum is building. This year, the signal was clear: Activity remained steady overall, pricing held firm, and the top of the market delivered one of its strongest winter performances in recent memory. And the Mamdani effect? As you will see throughout this newsletter and summarized below, we have not seen any indications of that.

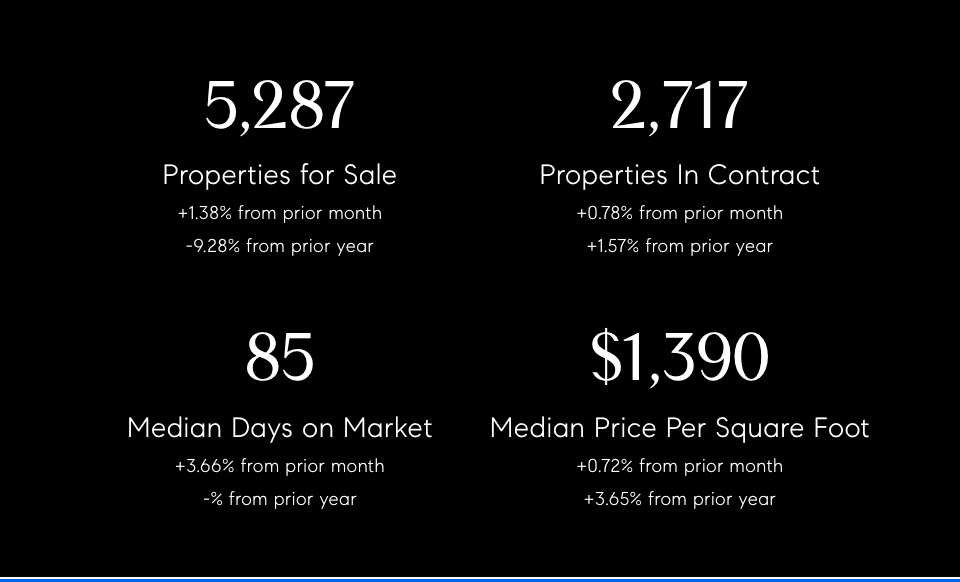

The broader numbers point to a market that is stable, disciplined, and increasingly segmented. Median price per square foot came in at $1,379, essentially flat month over month and modestly higher year over year, indicating that pricing continues to hold even as buyers remain selective. Days on market ticked up slightly but remain meaningfully lower than last year, demonstrating that most serious sellers are still finding buyers when expectations are realistic. Inventory edged higher from January but is still down nearly 10% year over year, keeping competition intact for well-priced product. The takeaway is straightforward: Manhattan is not surging, but it is clearly not soft. It is trading steadily with some pockets of real urgency.

The clearest evidence is at the top of the market. February recorded roughly $1.38 billion in luxury contracts, with 123 deals signed at $4 million and above and 13 at $20 million or more. That is a sharp increase from the same period last year and underscores how active the ultra-high-end segment remains.

Much of that momentum centered on specific buildings. 1122 Madison Avenue emerged as one of the defining stories of the month. Despite launching sales discretely only in mid-January (with no public facing marketing), the boutique Upper East Side condominium quickly generated contracts for most of its inventory, averaging more than $5,400 per square foot, with several deals above $20 million, including the $89M penthouse.

Other standout contracts highlighted both new development demand and buyers’ continued appetite for legacy properties. A Gilded Age townhouse at 15 East 63rd Street went into contract asking $39.5 million, while a full-floor residence at 175 Fifth Avenue secured a deal near $25 million, reinforcing demand across both historic and newer product. Weekly reporting throughout February showed similar strength, including multiple weeks with more than 30 contracts signed at $4 million and above and several eight-figure deals concentrated on the Upper East Side and in Flatiron.

This activity also effectively puts to rest speculation around the so-called Mamdani Effect. Concerns that political rhetoric or shifting sentiment would sideline affluent buyers have not materialized. If anything, signed contracts at the top of the market continue to outpace the broader market, reinforcing how insulated the luxury segment in Manhattan and Brooklyn remains.

The takeaway from February is straightforward. Manhattan remains a segmented market, but momentum is real. The luxury tier is active, new development is gaining traction, and properly priced resale inventory continues to trade. With inventory still tight heading into spring, the next two months will likely determine whether February’s strength turns into sustained acceleration.

Best Wishes,

Boris Fabrikant, Esq and Collin Bond, Esq.

Manhattan Market Recap

February 2026